![Pay Cat Logo New 2.png]](https://www.paycat.com.au/hs-fs/hubfs/Pay%20Cat%20Logo%20New%202.png?height=50&name=Pay%20Cat%20Logo%20New%202.png)

This article applies to any business with 19 or less employees (eligible business) who will commence reporting STP events from 1 July 2019 and up to 30 June 2021.

N.B. This article is no longer relevant, and for updated information pertaining to closely held employees on or after 1 July 2021 should be accessed from here.

What is a Closely Held Employee?

A closely held employee (payee) is one who is not "at arm’s length". This means they are directly related to the entity from which they receive payments. Examples include:

- family members of a family business;

- directors or shareholders of a company;

- beneficiaries of a trust.

The ATO have allowed a later reporting start date for any eligible business with closely held employees. Specifically, you will not need to report closely held employees through STP in the 19/20 financial year. In response to the COVID-19 crisis, the ATO have now extended the exemption deadline from 1 July 2020 to 1 July 2021.

To clarify, this does NOT mean you are exempt from STP reporting altogether. You must still report all other employees through STP commencing from the first pay run with a pay date on or after 1 July 2019. If you have been granted a deferral date from the ATO then you would commence reporting from such deferred start date.

This payroll software has been ready for STP reporting from 1 July 2018 and, as such, employers will not be granted a deferral from the ATO for reasons pertaining to the software not being ready.

If you are unsure of whether any employee in your business is deemed a closely held employee, you should obtain advice from the ATO.

Setting up a Closely Held Employee

The steps undertaken to classify an employee as closely held is as follows:

- Access the specific employee's file;

- Click on the employee's Pay Run Defaults menu;

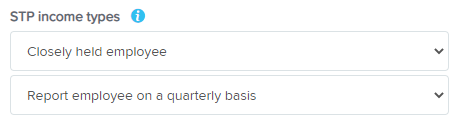

- Scroll to the bottom of the screen where you will see the STP income types field.

- Select 'Closely held employee', and select to report either on a quarterly or per-pay run basis.

If the reporting setting 'Report employee on a quarterly basis' is used, the employee will not appear in STP events created thereafter. N.B. As this exemption only applies from the 19/20 FY, selecting this setting prior to this and lodging an STP event in the 18/19 FY will NOT remove the employee from the STP event. This means that you can update employees now without having a concern that they will be removed from lodgements in the 18/19 FY.

Dealing with scenarios where employees have incorrectly been marked as closely held or an employer has forgotten to classify an employee as closely held

If an employee has incorrectly been classified as a closely held employee, follow these steps to correct the issue:

- Select a different option for the employee's STP Income Types field (from the employee's Pay Run Defaults page) and click on 'Save';

- Create and lodge an Update Event. This will include the incorrectly classified employee in the event and ensure they are being reported.

- Pay event lodgements thereafter will automatically include the employee if they were paid.

If an employee has not been classified as a closely held employee (and should have been), and as a result, has been reported to the ATO through STP you will need to get in contact with the ATO to rectify this as "reversal of events" are not catered for with the ATO.

To ensure subsequent events do not include the closely held employee, ensure you follow the instructions for "Setting up a Closely Held Employee" (above).

We have Closely Held Employees but still want to report them through STP. Can we do this?

Yes, you absolutely can! Simply select the option 'Report employee each pay run' from the employee's STP Income Types field from their Pay Run Defaults page after selecting 'Closely held employee', and the employee will be reported in STP events.

We have reported Closely Held Employees via STP but have changed our mind and want to issue them payment summaries instead. Can we do this?

No. If the employee has been included in any pay events for that financial year, you will not be able to generate a payment summary for them. This is to prevent businesses from potentially double reporting where they have been reporting through STP, then mark an employee as closely held during the financial year and subsequently issue a payment summary without reversing reported earnings. Essentially, once a closely held employee is reported through STP, the system will not allow you to stop reporting via STP during that financial year, even if you can otherwise claim an STP reporting concession.

Closely Held Employees & Payment Summaries

Eligible businesses not reporting closely held employees through STP must follow 'old school' end of financial year processes for those employees. What does 'old school' mean? It means closely held employees will need to be provided with a payment summary and a payment summary annual report must also be lodged with the ATO. This must only be done for closely held employees not reported through STP.

If you have any questions or feedback, please let us know via support@yourpayroll.com.au.